Silo Finance — Weekly Risk Report (Week 1)

This report provides a structured weekly risk review of lending markets on Silo Finance. The objective is to identify pools with elevated liquidation, oracle, and liquidity risk under stressed market conditions.

For Week 1, markets are divided into two segments:

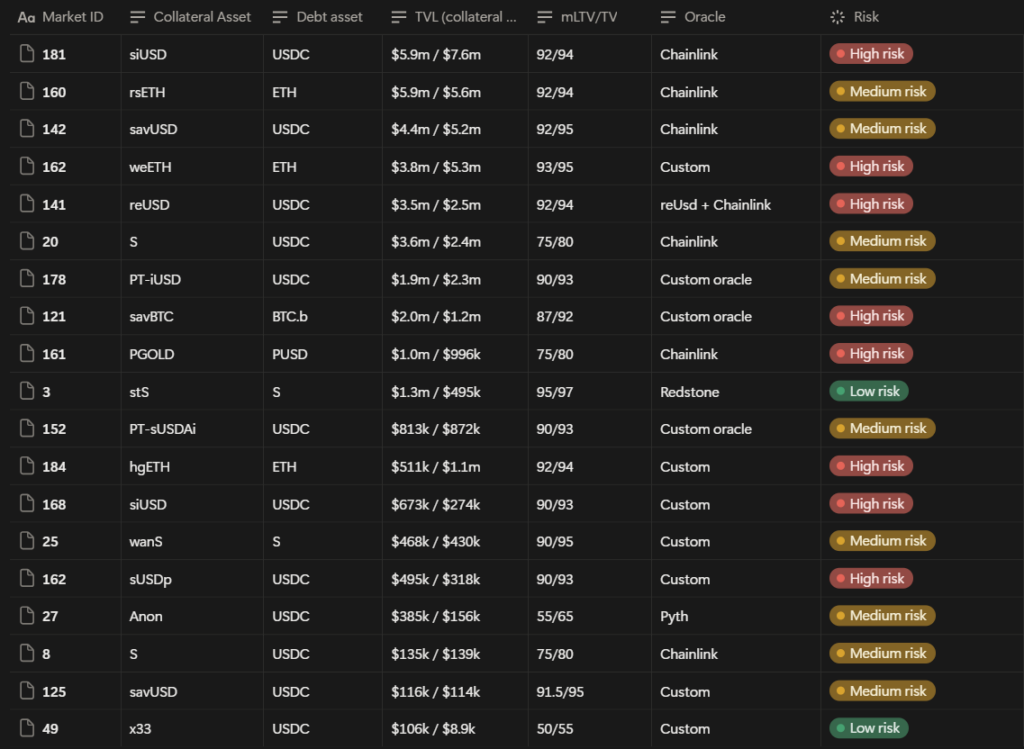

Section A: Core Pools (> $100K collateral deposits)

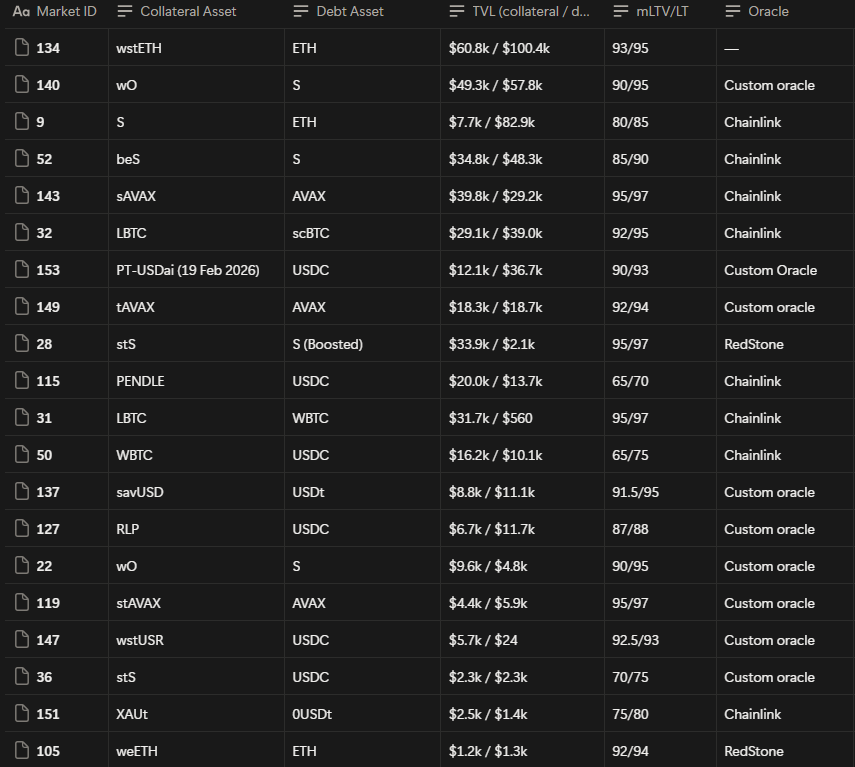

Section B: Long-Tail Pools (< $100K collateral deposits)

Risk labeling excludes smart contract exploit risk and focuses on market structure, liquidity depth, oracle design, and liquidation viability.

Section A (>$100K Collateral)

Section B (<$100K Collateral)

High Risk Methodology & Rationale

In this section, we provide a pool by pool breakdown of all Section A markets labeled High Risk, explaining the specific failure modes and risk drivers for each pool (excluding smart contract exploit risk).

Our risk classification is based on a multi factor framework that includes:

- Oracle design and price feed freshness

- On chain liquidity depth and exit capacity

- Market size and effective TVL concentration

- Borrow utilization and available liquidity buffers

- Collateral volatility and correlation risk

- Parameter sensitivity (mLTV / liquidation thresholds)

- Structural and market specific constraints

We also run forward looking scenario analysis using our internal monitoring and stress testing tools to evaluate how each pool behaves under adverse market conditions.

High Risk Pools — Detailed Breakdown

Pool 181 — siUSD / USDC

Key Observations

Total siUSD DEX liquidity: ~$4M

Total siUSD used as collateral: ~$5.9M

Documented siUSD depeg history

Collateral size exceeds reliable exit liquidity

Primary Risk Drivers

Liquidation cascade risk under stress conditions

siUSD depeg → liquidation failure → bad debt formation

Potential death spiral scenario if:

price deviates,

liquidation incentives are insufficient,

gas costs spike simultaneously

Failure Mode

If siUSD depegs and liquidators cannot exit positions profitably due to shallow liquidity and execution costs, liquidations stall and protocol bad debt accumulates.

Suggested Actions

Increase siUSD DEX liquidity depth

Reduce siUSD deposit cap

Temporarily reduce mLTV to ~80% until liquidity and stability metrics improve

Pool 168 — siUSD / USDC

Key Observations

siUSD collateral exposure remains elevated

Known historical depeg behavior

Primary Risk Drivers

Same structural exposure as Pool 181

Liquidation cascade and death spiral dynamics

Liquidity vs collateral imbalance risk

Suggested Actions

Increase siUSD liquidity depth

Reduce deposit caps

Lower mLTV to ~80% until stabilization

Pool 162 — weETH / ETH

Key Observations

weETH DEX liquidity on Arbitrum: ~$3M

weETH collateral deposited: ~$3.8M

Oracle-dependent pricing

Primary Risk Drivers

Oracle freshness / update lag risk

Liquidity thinner than collateral base

LST derivative pricing sensitivity

Failure Mode

Oracle lag or stale price combined with thin exit liquidity can produce under-liquidation and bad debt.

Suggested Actions

Reduce mLTV to ~85%

Strengthen oracle freshness guarantees

Add oracle redundancy if possible

Pool 141 — reUSD / USDC

Key Observations

reUSD DEX liquidity (Avalanche): ~$1.4M

reUSD collateral deposited: ~$2.5M

Oracle-dependent valuation

Primary Risk Drivers

Oracle freshness dependency

Liquidity depth insufficient vs collateral

Stablecoin-style peg fragility risk

Failure Mode

Oracle lag + liquidity gap → liquidation slippage → bad debt risk.

Suggested Actions

Reduce mLTV to ~85%

Improve oracle update guarantees

Monitor peg deviation thresholds

Pool 121 — savBTC / BTC.b

Key Observations

savBTC DEX liquidity: < $100K

savBTC collateral deposited: ~$2M

Custom oracle pricing

Primary Risk Drivers

Extremely low exit liquidity

Custom oracle trust assumptions

Depeg and death spiral risk profile

Failure Mode

Collateral cannot be liquidated at scale → liquidations fail → systemic bad debt.

Suggested Actions

Freeze market temporarily

Reopen only after:

liquidity depth improves materially

oracle robustness is validated

Pool 161 — PGOLD / PUSD

Key Observations

Chainlink oracle tracks XAU forex price

Collateral asset = PGOLD token

Oracle tracks reference asset, not token market price

Primary Risk Drivers

Oracle/reference mismatch risk

Peg trust assumption between PGOLD and XAU

Token-specific deviation risk not captured by oracle

Failure Mode

If PGOLD deviates from gold price while oracle tracks XAU, protocol may overvalue collateral → bad debt risk.

Suggested Actions

Validate peg mechanism transparency

Add token-specific pricing safeguards

Consider haircut or reduced mLTV

Pool 184 — hgETH / ETH

Key Observations

Vault-based asset used as collateral

Oracle relies on NAV valuation

NAV potentially manipulable depending on vault mechanics

Primary Risk Drivers

NAV manipulation risk

Oracle reliability concerns

Valuation attack surface

Failure Mode

Inflated NAV → overvalued collateral → under-liquidated positions → protocol bad debt.

Suggested Actions

Freeze market until valuation methodology is fully verified

Require hardened oracle design

Add conservative valuation buffers